Why A Global Standard For Digital

Receipts Is Required

By

Mark Johnson (@ReceiptReliance)

In most countries

around the world, the standard practice for issuing itemised receipts is for

merchants to produce a piece of paper with detailed purchase information on it

and then give it to their customers. Simple. It can be hand written or machine

printed, basic in design or elaborate, monochrome or colour - it doesn't

matter. The procedure is the same.

These days most

people would agree that digital

receipts are the future. However, the term 'digital receipts' has become a bit

of a catch-all for many different types of solutions. This begs the question: how

do we go from paper to digital without turning a relatively simple process into

a complicated one for consumers and merchants?

Well,

agreement on a standard would be very useful.

I'm not

suggesting uniformity with regard to the appearance of receipts; I think

control of that should be left to each individual merchant. Many will be keen

to reinforce their brand via consistent visuals.

Rather, I'm

talking about a standard in relation to what we do with digital receipts when

they are created, and where we store them.

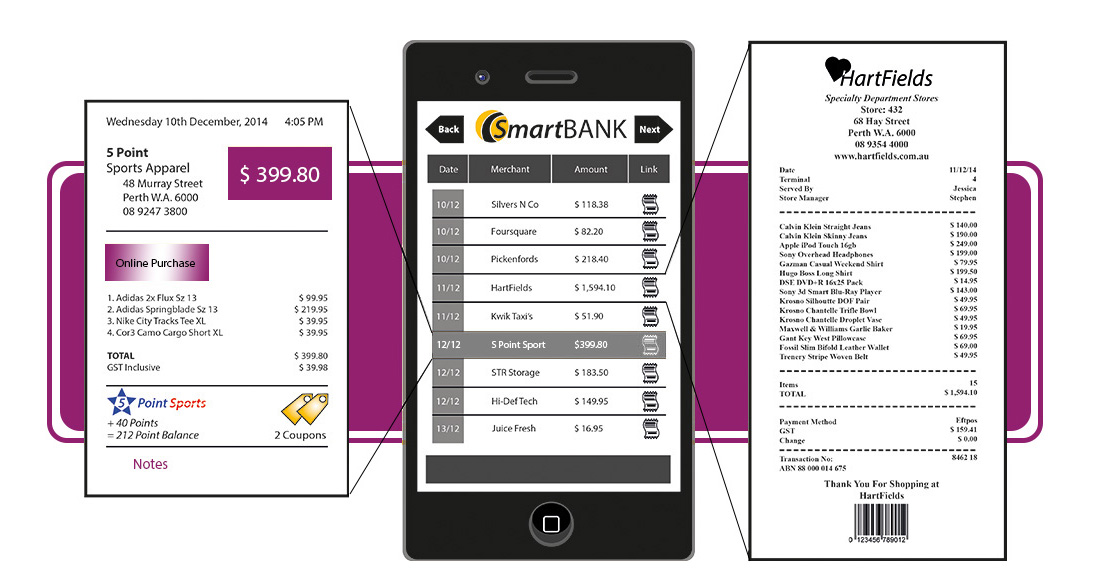

For some

time now I've been promoting a solution whereby a digital receipt is created at

the point of sale, it is linked to the associated payment transaction, and then

made available to consumers via their online or mobile banking applications.

This TechCrunch article provides more detail. Connecting the

payment transaction and the itemised receipt at the point of sale makes sense for many valuable reasons.

Remember,

· the

payment transaction records the total cost for a purchase; the merchant receipt

records the list of items that comprise that purchase. Two sides of the same

coin.

· both

are generated at the time of sale, but then they are separated; the payment

transaction is sent to our bank while the merchant receipt is given to the

customer, who may then need to reconcile them again for expense claims or tax

purposes. Matching them up can be an onerous task and not without error, and it

does make you wonder why they are still being separated in the first place.

While

consumers have control over where they choose to store their paper receipts, or

photos thereof, they don't always have that luxury with the digital version. Mostly,

they are at the mercy of whatever solution merchants choose, so that could mean

their email inbox, a cloud account (per merchant), or perhaps their smart

phone. If it's their phone, that could mean a specific digital wallet, any

number of merchant or receipt apps, or maybe a sms.

Given the

variety of locations they might be sent to, finding and/or consolidating digital

receipts could become quite a task for consumers. Replacing one, simple,

practice with a multitude of different ones adds complexity to receipt

management. It is not going to make our lives easier, which is one of the main aims,

isn't it?

If we had a global

standard for digital receipts there would be consistency across the shopping

experience for consumers. We could make a non-cash payment for a purchase

almost anywhere in the world and have full confidence that an original, authentic,

intact digital receipt from the merchant, will be available to us via our online

or mobile banking applications.

A standard would

level the playing field for merchants. In my experience most are very

interested in offering digital receipts to their customers, but are hesitant to

dive in just yet. Some reasons for this include concerns not only about cost,

data security, and customer privacy, but also product selection; they're unsure

which one will serve them best in the long run. We were met with keen interest

and received some great feedback when describing a 'point of sale to customer

bank' solution. In addition to acknowledging many advantages for themselves,

most said that they think their customers would love it.

With the onset

of Open Banking , we are seeing a lot of innovative development taking place, some

of which is focussed on applications that will provide consumers with an aggregated

view of their finances. Dashboards displaying accounts and transactions from

different banks on the one screen are giving consumers a much better picture of

what's happening with their money. Imagine then, if it were standard to have

receipts attached to transactions; the receipt could be sourced at the same

time a transaction is pulled in - easy! Currently the ability to do this is

somewhat hampered due to the myriad of receipt storage locations, some

accessible and others not so much.

A recent article from Acuity featuring discussions with Chris Jordan FCA, Commissioner of the Australian Tax Office, provided a

look at how the ATO has been travelling over the past few years, and what areas

of innovation it might cross paths with going forward.

From the

article - "Jordan has always spoken

enthusiastically about technology’s potential to ease small business

interactions with the ATO." saying that it will inevitably lead

to "a future where more

businesses can tie their accounts directly into ATO systems."

It would

certainly be convenient if it were standard to connect receipts to

transactions.

Chris Jordan

goes on to say, “If we can tap into natural systems

so that small businesses can comply with their obligations without doing anything

special, that’s a great outcome.”.

A digital

receipt standard could be backed by regulation to ensure compliance and quality

control. In my view, such regulation should have a primary focus on the

following:

·

Privacy of the consumer - based on an acceptance that the receipt

data is owned by the consumer and can be shared or utilised as they see fit.

·

Integrity of the data - must be assured from

the point of creation through to transport and then storage.

·

Electronic payment system policy - regarding payment system participants' provision for

and handling of receipt information, when payment system infrastructure is

being utilized.

To assist the

adoption of a standard, I think it's important to keep the approach as simple

as possible and to stay focused on the core proposition of simply delivering

digital receipts to consumers. It's easy to get distracted with value adds

which can introduce unnecessary complexity and might even end up having the

opposite effect to what was intended. Our informal discussions with merchants provided

useful insight backing this up. For example, incorporating loyalty features as

part of the minimum package can in some cases be a deterrent; some already have

successful programs in place while others are just not interested, preferring to

encourage customer loyalty through keen pricing policies.

In order to

shine through and become a global standard for digital receipts, the successful

solution will have the following attributes:

·

Consumer

-first approach

·

Seamless

in operation

·

Privacy

of the consumer ensured

·

Convenient

access from consumer

standpoint

·

Integrity and security of the data ensured

·

Reliability

·

Payment

method/device agnostic.

Natural

selection has begun for digital receipts with many early solutions giving way

to those more popular in the marketplace. Some factors contributing to their

lack of success might include the requirement for consumers to share personal

information, added friction at the checkout, additional cost to merchants, or perhaps

because the solution was device specific. Whatever the reason, surviving

solutions continue to evolve and new ones continue to arrive.

I think it's

only a matter of time before we start to see the emergence of a standard and

it's interesting to note a shift in direction towards financial institution

involvement. The past few years have seen ongoing efforts by banks and ADIs to

provide enhanced transaction detail to their customers, and for purchase

transactions, there is really no better source of detail than the itemised

receipt.

A digital

receipt standard will have far reaching benefits for all of us. As technology

improves, so too does the opportunity for stakeholders in the banking, payment

and retail space to further engage with one another to accelerate this natural evolution.

We welcome your feedback, suggestions,

comments and/or support.